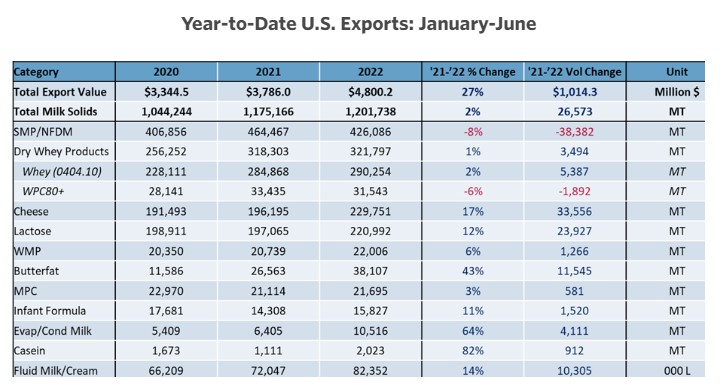

Cheese, whey drove U.S. dairy exports to finish the first half positive in both volume and value.

U.S. dairy exports jumped sharply in June (+9% by volume on a milk solids equivalent basis) despite growing uncertainty in the macroeconomic environment. The rapid expansion of cheese exports, particularly cheddar, remains a consistent storyline for U.S. dairy in 2022. U.S. cheese exports grew by 31% (+10,349 metric tons, or MT) year-over-year in June.

While cheese exports were the stars of the show, they were by no means alone. Exports of U.S. whey products increased by 23% (+10,531 MT), as Southeast Asian buyers secured supplies and volumes held steady to China – the largest single whey importer in the world by a wide margin. Lactose exports saw similar levels of growth (+22%, 7,426 MT).

NFDM/SMP was the only major product to see an export decline in June (-14%, -11,288 MT). But as we discussed in last month’s write-up, the primary obstacle to growing NFDM/SMP exports remains a lack of supply, as U.S. milk powder production trailed prior year levels by 8% (-224,868 MT) over the past 12 months.

Beyond the major categories, the U.S. expanded its portfolio to include gains in milkfat-heavy products. Butter jumped 63% (+2,272 MT), AMF more than tripled (+225%, +1,695 MT), WMP climbed significantly (+83%, +1,695 MT), and even evaporated/condensed milk saw substantial growth (+77%, +883 MT).

Overall, June’s data confirms that even if domestic consumption slows with economic turbulence, the U.S. dairy industry is growing its presence in the international market.

Let’s dive a bit more into why U.S. exports performed so well, particularly in cheese and whey.

Cheese: Available Supply + Advantageous Prices + Demand Growth = Export Boom

Through the first half of 2022, U.S. cheese exports grew by 17% (+33,556 MT), easily on pace to smash the previous annual record. This rapid expansion comes after three-and-a-half years of relatively little growth. From January 2018 through June 2021, U.S. cheese exports only saw a single month where annualized exports fell outside the relatively narrow band of 340,000-365,000 MT. June’s trade figures show U.S. cheese exports grew to an annualized volume of over 436,000 MT.

So, what’s driving this rapid success in cheese exports?

First, the U.S. has supplies available to export, unlike many of its competitors. Despite limited milk production growth in the U.S., cheese production has managed to expand. Through May, U.S. cheese production is up 2.5%, while domestic consumption is up only 1.7%. Indeed, domestic consumption of American-type cheeses is actually down 1.5%, creating an opportunity for the near doubling of cheddar exports (+96%, +22,006 MT).

Second, U.S. cheese has been relatively affordable on the global market, both on a spot basis and in futures markets for the majority of the first half of the year. This gap between U.S. cheddar prices on the CME and New Zealand prices on the GDT (coming off the lowest milk production season in four years) supported gains in U.S. market share in Japan and Korea, two of the most highly contested cheese markets.

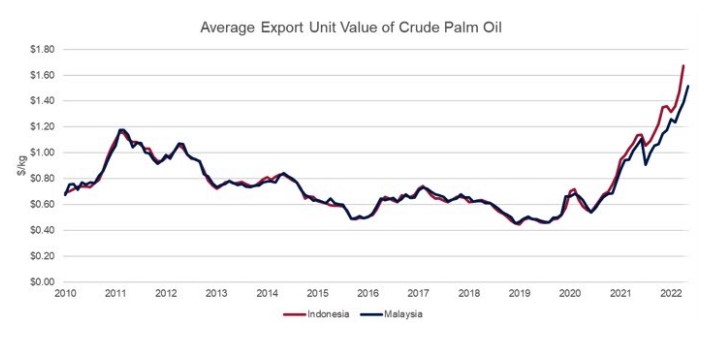

Pricing factors have also favored U.S. suppliers in key buying regions like Mexico and Central America, where U.S. exports grew by 15,848 MT combined in the first half of 2022. Today, U.S. natural cheese is virtually equal in price to cheese analogues, a traditionally much cheaper alternative that uses palm oil instead of dairy fats. With soaring palm oil prices (see chart below), the incentive for end-users to trade down to analogues has weakened significantly.

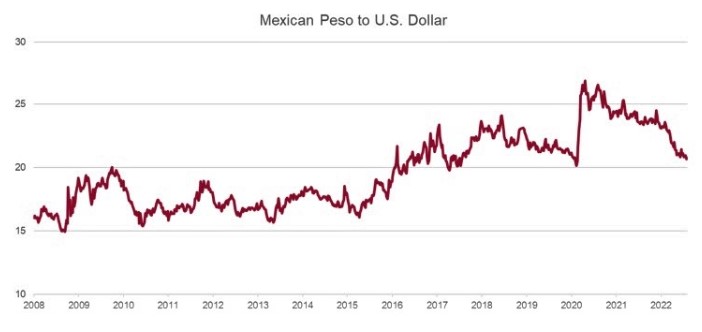

Finally, the competitiveness of U.S. natural cheese compared to analogues is boosting demand in Latin America at a time when a strengthening peso is raising purchasing power for imports and local milk production remains weak. All of it is contributing to rising demand in the region.

Fundamentally, the U.S. having supplies available for export combined with advantageous prices and growing import demand equals an export boom in cheese, despite the many headwinds of shipping, economic uncertainty, and still historically high prices.

Looking ahead, U.S. cheese exports are well placed to continue growing in the near term. The peso is holding steady and even while palm oil prices and competitor prices have come down in recent weeks, exports should keep expanding through the second half of the year since these changes will take time to work through the system.

The major wildcard is Europe. EU27+UK milk production continues to lag, but with concerns over natural gas shortages come winter, the cheese vat is likely to look much more appealing for local processors than a gas-intensive dryer, potentially increasing competition in cheese later in the year.

Whey and Lactose: Improved Shipping and Growth to SEA and China

U.S. whey shipments posted their best month of the year in June, with year-over-year volume up 20% (+10,182 MT) to 62,321 MT. Lactose volume rose 22% (+7,426 MT) to 41,642 MT.

June saw strong gains in whey shipments across geographies, including Southeast Asia (+3,628 MT), Canada (+2,668 MT), South America (+1,938 MT) and Japan (+1,688 MT). That stellar performance lifted year-to-date U.S. whey exports into the black, with total U.S. shipments up 1% in the first half, compared to the first six months of 2021.

The rebound in Chinese pig prices that began in mid-April and peaked in July likely also supported June whey export volume. U.S. whey exports to China (excluding WPC80+) grew 6.5% (+1,618 MT) with gains in sweet whey and permeate. At 26,638 MT, it was the most whey (excluding WPC80+) the U.S. ever shipped to China in a single month—even during the months of herd rebuilding from African Swine Fever.

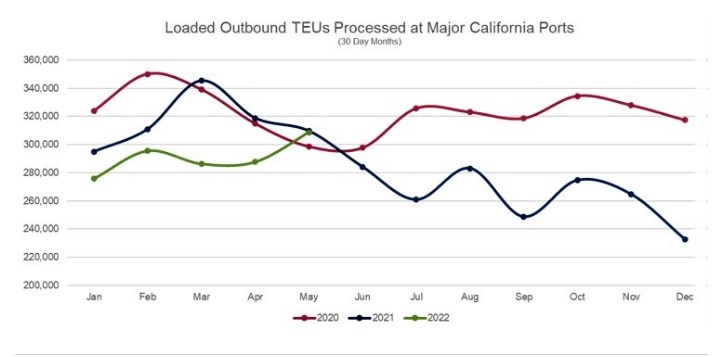

But more broadly, the recovery in U.S. shipping is what helped lift overall U.S. whey and lactose volumes in June. The many mitigation measures taken by players throughout the U.S. supply chain—including the pop-up container facilities, threats to implement dwell time fees to ocean carriers, and the implications of the Ocean Shipping Reform Act—are beginning to make a difference as delayed product secures passage aboard ocean vessels.

After declining for most of the final three-quarters of 2021, the number of loaded outbound TEUs leaving major California ports has been slowly ticking upward this year. In May, loaded outbound TEUs matched the previous year for the first time in nearly a year.

While the West Coast dockworkers contract remains a big shipping unknown, the improvement in container flow bodes well for U.S. dairy export efforts heading into the back half of 2022—particularly as more attention is paid to correcting additional supply chain choke points. Economic growth and inflation (from dairy input costs to retail prices) will continue to create export headwinds, but the supply chain arguably is looking up for the first time since before the pandemic.

Provided by U.S. Dairy Export Council