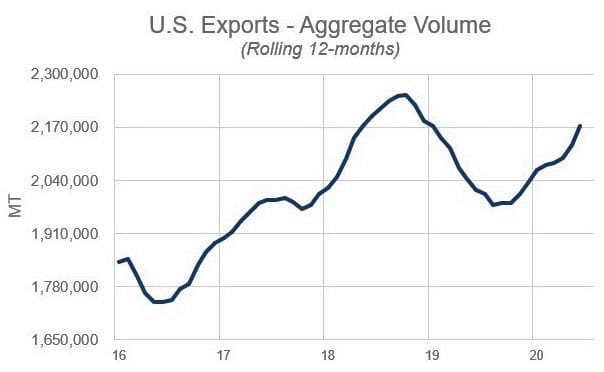

U.S. dairy exports in June were up 28% by volume and 22% by value, capping a first half of double-digit growth. This year’s gains have been all the more impressive in that they were achieved during one of the most disrupted dairy trade environments in history.

In June, U.S. suppliers shipped 206,411 tons of milk powders, cheese, whey products, lactose and butterfat, the most (on a daily-average basis) since April 2018. The value of all exports was $583.7 million.

On a total milk solids basis, U.S. exports were equivalent to 17.7% of U.S. milk solids production in June, the highest rate since April 2018. In the first half of the year, exports were 15.8% of production, up from 14.1% in the first half of 2019.

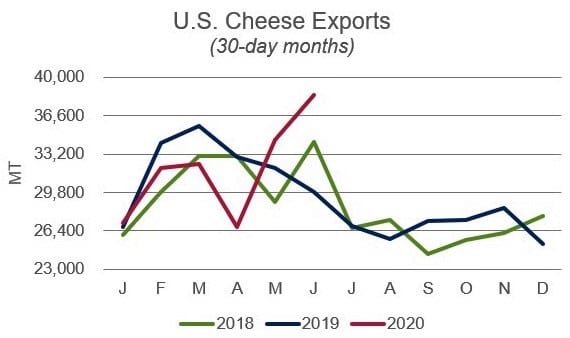

Headline highlights in June included record cheese exports, continued robust sales of nonfat dry milk/skim milk powder (NDM/SMP), ongoing recovery of whey sales, and record shipments of fluid milk/cream. Overall volume gains vs. a year ago came from Southeast Asia, China and the Middle East/North Africa (MENA) region, plus a welcome improvement in sales to Mexico.

Cheese exports in June were 38,427 tons, 29% more than last year and the most ever. Much of this volume represents deals booked in April and May when U.S. cheese prices were at historic lows. The unit value of shipments was just $3900/ton, the second lowest over the last nine years.

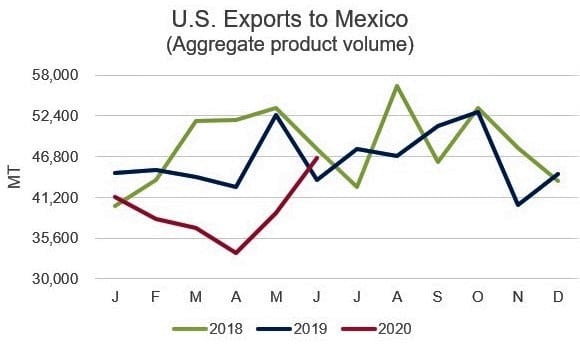

Mexico came back to buy the most cheese in two years, posting a 62% gain compared with a year ago. Sales to South Korea also were strong, up 56%, and shipments to China more than doubled.

Exports of NDM/SMP topped 75,000 tons for the second straight month, coming in at 75,831 tons in June, up 77% from a year ago. Sales to Southeast Asia were lower than the previous two months, but still more than double the June 2019 volume. Growth came from Malaysia, the Philippines, Indonesia and Vietnam. Meanwhile, Mexico made its largest purchases in eight months, posting a 13% gain vs. a year ago. Mexico buying was encouraging, on the heels of a 21% decline in the first five months of 2020.

U.S. suppliers also sold nearly 10,000 tons combined to China and the MENA region (mostly Egypt); a year ago they sold less than 800 tons to the two markets. In the first half of the year, exports to the MENA region were up more than five-fold.

U.S. whey exports continued to trend higher on the strength of recovering sales to China, the top market for U.S. whey. Total whey shipments were 44,794 tons, up 8% from last year and the most since August 2018. Dry whey exports were up 42%. Sales of whey protein isolate (WPI), though less than the November-April levels, were still 30% more than last year. With strong global demand for protein, U.S. WPI exports were up 27% in the first half of the year.

China’s whey needs are expanding, largely due to swine herd restocking following last year’s African Swine Fever outbreak. June volume was the most since May 2018, and up 79% from last year. This offset a continued slump in whey sales to Mexico (-52%).

U.S. suppliers exported 13.4 million liters of fluid milk/cream in June, up 17% from last year and the most ever. Sales to Taiwan were a record high, while shipments to Canada doubled.

Lactose exports in June were 33,184 tons, on par with prior months but down 4% from last year. Shipments to China continued to improve (+19%), while sales to Southeast Asia were up 10%. In both markets, demand for use in infant formula was strong.

Among other products, shipments of milk protein concentrate (+28%), butterfat (+15%) and food preps/blends (+17%) were higher. Volume of whole milk powder (-2%) continued to lag.

Source: U.S. Dairy Export Council